Qualified Small Business Stock (QSBS) is some of the most tax-advantaged stock you can hold, yet few people know about it. If you’re a founder, early employee, or investor, you can potentially save millions of dollars by understanding the implications of QSBS.

In this article I will discuss the following:

- History of QSBS

- QSBS Tax Savings

- Requirements for QSBS

- Section 1045 Rollover (applicable if you don’t meet the five year holding period, explained below)

I recently sold shares in a company I co-founded and spoke to more than two dozen accountants in the process. I’m summarizing my findings and experiences in the article below. As such, the information in this article is not formal tax advice. I recommend you speak with your accountant prior to making any decisions.

History of QSBS

Section 1202 is the section of the tax code that outlines the QSBS tax exclusion. It was added to the tax code in 1993 to encourage individuals to invest in new ventures, far before the creation of Silicon Valley as we know it today. The act, however, failed to provide the intended incentive of spurring investments in new ventures.

Over the past three decades, a number of tailwinds have propelled QSBS back into the limelight. Congress reduced the tax on long-term capital gains in 1997, increased the tax savings of QSBS incrementally until 2010, and finally reduced corporate taxes from 35% to a flat 21% in 2017. These three forces have made QSBS far more relevant today than in the past.

QSBS Tax Savings

Under Section 1202, your gains from selling QSBS may be eligible for up to 100% exclusion from federal and state taxes. This exclusion is limited to the greater of $10 million or 10 times your cost basis during a liquidity event.

For instance, the excludable amount for a founder may be on $10 million of gain, while the exclusion for a VC may be much greater. If, for instance, a VC invests $20 million, the VC may obtain an exclusion for $200 million of gain. See the “Scenario Table” in the Appendix for more examples. Please also note that if you end up selling your shares in multiple tranches over multiple years, the excludable amount might vary. Reference this article for further details.

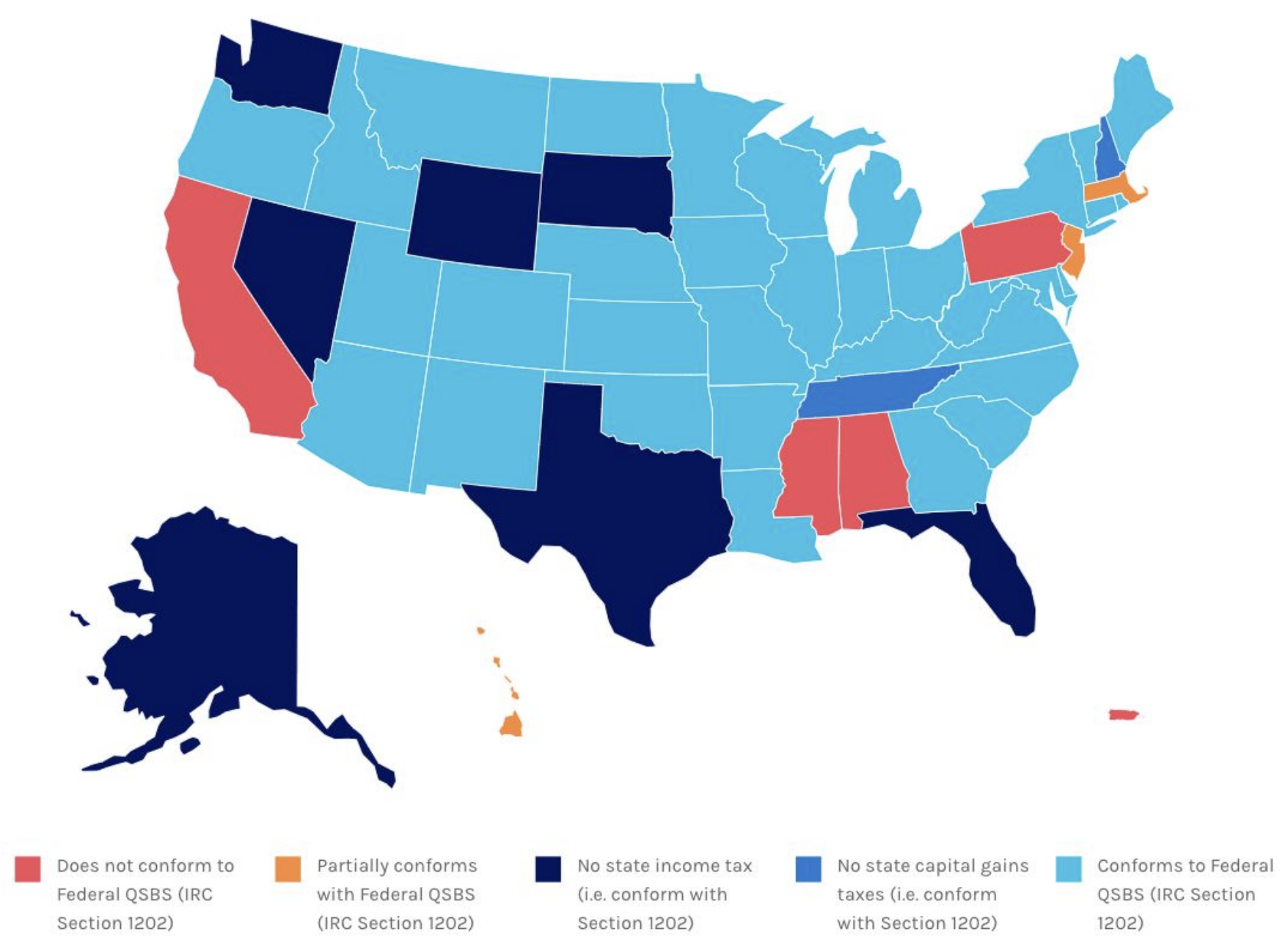

If you qualify for a QSBS tax exclusion, you are 100% exempt from federal taxes. The current federal tax rate is 23.8% (20% federal + 3.8% medicare). This means you can save 23.8% in long-term capital gains that you would have been subject to otherwise. Depending on which state you live in (not which state the company is incorporated), you may qualify for state-level exclusion as well. States typically fall into one of four buckets:

- States with no individual income tax or no capital gains tax. These states are QSBS compliant by default.

- States that follow the federal tax code and waive state taxes if an individual meets the federal-level QSBS requirements. These states are also QSBS compliant.

- States that have their own QSBS exclusion statues.

- States that do not recognize QSBS in any way, shape, or form (California notably falls in this bucket).

I’ve provided a chart of applicable QSBS treatment in each of the 50 states and District of Columbia in the Appendix.

Requirements for QSBS

For your stock to qualify as QSBS, you must meet certain requirements at the time of your stock issuance, and others during your entire holding period of the stock. If you sell QSBS, you must report the entire gain as a long-term gain on your Schedule D, and enter the allowable exclusion as a loss below the entry for the gain.

Requirements that must be met on the date of issuance:

- Corporation issuing the stock must be a domestic C-Corp (and the stock must be issued after August 9, 1993)

- You must acquire your stock directly from the company for money, property, or services. The only exception is if you acquire the stock by gift or inheritance. In this case, you are treated as having acquired the stock in the same manner as the original owner.

- Note: do not contribute the stock to a family LLC, limited partnership/trust, or to an LLC organized to manage the sale of your stock. This will disqualify the stock as QSBS.

- Corporation must have assets of $50M or less at the time you receive your shares (or exercise your options).

- Note: this is a continuous requirement and if at any point the assets of a corporation exceed $50M, the corporation can never again issue QSBS (even if the assets are below $50M on the date of the subsequent issuance).

- Note: the assets of the corporation must not exceed $50M even after taking into account amounts the corporation received in the current issuance. If, for instance, a company has $40M in the bank and is raising a $20M Series B, none of the newly issued Series B stock will be QSBS.

- You must determine your stock issuance date. This is critical for three reasons:

- Starts the clock for purposes of the five-year holding period requirement. In order to be eligible for the tax exemption outlined above, you must have held on to your stock for a minimum of five years. If you do not meet this minimum requirement, you can employ a Section 1045 rollover (described below) to extend your holding period.

- Note: this requirement is yet another reason why you should early exercise your options and file an 83(b). Early exercise allows you to 1) start the one year holding period for long-term capital gains treatment, and 2) start the five year holding period for Section 1202. If you don’t file an 83(b) election, the clock on long-term capital gain only begins when your shares vest – so if there are multiple vesting dates, you will have multiple clocks to monitor for long-term capital gain – and, if eligible, QSBS. An unexercised option or warrant is not considered QSBS, even if the underlying stock would meet the definition of QSBS.

- Note: for stock acquired through the exercise of an option, the company must pass the “$50M asset test” on the date of your exercise, not on the date of your grant. Similarly, for stock acquired through the vesting of RSUs, the company must pass the “$50M asset test” on vesting, and your five year holding period begins on vesting, not on grant.

- Note: if the stock was received as a gift, inheritance, or as a distribution from a partnership, the acquisition date is the date on which the transferor acquired the stock.

- Determines whether gain from the sale of the QSB stock is eligible for a 50%, 75%, or 100% federal tax exclusion.

- 50% federal tax exclusion for stock issued before February 18, 2009

- 75% federal tax exclusion for stock issued between February 18, 2009 and September 27, 2010

- 100% federal tax exclusion for stock issued after September 27, 2010

- Marks the date on which the company must have $50M or less in assets.

- Starts the clock for purposes of the five-year holding period requirement. In order to be eligible for the tax exemption outlined above, you must have held on to your stock for a minimum of five years. If you do not meet this minimum requirement, you can employ a Section 1045 rollover (described below) to extend your holding period.

Requirements that must be met during the shareholder’s holding period:

- Corporation must be a C-corp for the entire holding period.

- The corporation must be an “active business” during the entire period you held your stock. This means that at least 80% (by value) of the assets in your corporation must be used to pursue business in industries other than the industries below. Note that if your business provides a service, then it most likely does not qualify as a qualified small business.

- Health, law, non-software engineering (civil, electrical, etc), architecture, accounting, actuarial science, performing arts, consulting, athletics, financial services, or brokerage.

- Banking, insurance, financing, leasing, investing, or similar business.

- Farming.

- Mining or natural resource production or extraction.

- Operating a hotel, restaurant, or similar business.

- Cash held for burn requirements generally qualify under this “active business” requirement. However, after two years, technically no more than 50% of the corporation’s assets can qualify under this exemption. While startups usually satisfy this requirement, it isn’t always clear how to apply the rule, especially if the startup retains significant cash following an investment (in other words, overfunded startups sitting on cash). If you’re like most startups and you’re burning cash to fund business operations you will most likely pass this check.

- If the corporation bought back 5% or more of its stock in the year before or after your stock issuance, your stock will not qualify as QSBS.

Section 1045 Rollover

In order to be eligible for preferential tax treatment under Section 1202, you must satisfy the requirements above and have held onto your stock for at least five years. If you have not met the five year minimum, however, you can employ a Section 1045 rollover to extend your holding period.

If you have held onto your QSBS for at least six months, you can sell your QSBS and roll the proceeds of the sale into another QSBS issuer without recognizing a gain under Section 1045. This is a similar concept to a Section 1031 exchange in real estate. Per Section 1045, you have 60 days from the date of the sale of your original QSBS to roll the sale proceeds into new QSBS. In general, you should roll all of the proceeds from your sale of original QSBS into the new QSBS. If you take any cash off the table after the initial sale, that amount would be subject to capital gains tax. The cost basis of the new QSBS is the same as the cost basis of the original QSBS, and the holding period from the original QSBS is counted towards the holding period of the new QSBS.

Consider the following scenario: you acquire 5M shares of QSBS from “Company A” on January 1st, 2010 for $0.00001 per share. Your original cost basis is $50 (5M * $0.00001). Assume you then sell these shares in Company A for $4M on January 1st, 2012, and then reinvest this $4M to purchase 2,000 shares of QSBS in “Company B”. Your holding period will pick up from where it left off and the cost basis for your new shares in Company B will be the same as the original cost basis for your shares in Company A ($50). If you then sell your QSBS in Company B at any point after January 1, 2015, you will be exempt from federal taxes for up to $10M of realized gain. This means you will not have to pay any federal taxes if you sell your shares in Company B for $10M or less.

Once you successfully conduct a Section 1045 rollover (described below) and have a combined holding period of at least five years, you are free to sell your shares and exclude any applicable gains under Section 1202.

Steps to Conduct a Section 1045 Rollover

These are the steps to employ a Section 1045 rollover, along with the documentation you need to maintain in the event of an audit.

- Maintain the following documentation from your original company:

- Original Stock Purchase Agreement between yourself and the issuing corporation. Ensure this agreement documents the cost basis (amount paid) of your stock.

- Proof of payment (for instance, a copy of the account statement reflecting that the funds left the account to pay for the stock).

- Share certificate(s).

- 83(b) election (if applicable).

- Domestic C-Corp incorporation documents (if you have access to these).

- Fundraising documents proving assets were under $50 million for the entire holding period (if you have access to these).

- Maintain documentation of your stock sale of the stock in your original company.

- Incorporate a new domestic C-Corp (I swear by Stripe Atlas) and maintain a copy of these incorporation documents.

- Execute a Stock Purchase Agreement between yourself and the new Corporation, and maintain documentation of this new stock issuance.

- File your 83(b) election for your new company. To do this, you must fill out 83(b) form provided to you by Stripe Atlas (or use this one from Fidelity), and mail it to the IRS with “Return Receipt Requested”. Save a copy of your receipt as this will be your proof that you mailed your 83(b) on time.

- Note: you also need to cut a check to your new company to purchase your shares in accordance with the 83(b). The strike price is typically $0.00001, so the purchase amount is typically on the order of $100. Document this check (for instance, retain a copy of the account statement reflecting that the funds left the account to pay for the stock).

- Open up a Business Bank Account (SVB has an existing partnership with Stripe Atlas).

- Create priced equity financing documents (I used this document generator from Cooley).

- Note: the financing note must be a priced equity note and not SAFE note. A SAFE note is simply a promissory note for shares at some point in the future and is not sufficient to restart the five year holding period.

- Upon completion of your priced equity financing documents, wire the proceeds of your original stock sale into your business bank account. Maintain documentation that you wired the proceeds of your original sale within 60 days of receiving the money.

- Record the Section 1045 Rollover on your Schedule D. First, report the entire gain in Part I if a short-term gain or Part II if a long-term gain. Then, directly below the entry you made in Part I or Part II, write the following: “Section 1045 Rollover”. Report the rolled-over amount as a loss in column (f).

- Maintain ongoing documentation that the new corporation meets all of the “active business” requirements outlined above. At a bare minimum you must maintain the following:

- Detailed Business Plan and Financial Model of how you plan to spend the funds.

- Document ongoing operational costs (I use Xero for accounting).

Thanks to Saureen Shah, Kojo Osei, Francisco Giminez, Bhaskar Ghosh, Andrew Bakst, Ayush Sood, Karanveer Mohan, Teddy Jungreis, Kunal Jain, Chase Johnson, Jason Gore, and Hyde Patterson for reviewing drafts of this article.

Appendix

Scenario Table

| Persona | Price Per Share (PPS) | Number of Shares | Cost Basis | Sale Amount | Excludable Amount Under QSBS |

| Founder | $0.00001/share | 5M | $50 | $15M | $10M |

| Investor #1 | $1.50/share | 500k | $750k | $50M | $10M |

| Investor #2 | $5/share | 1M | $5M | $55M | $50M |

| Early Employee #1 | $0.20/share | 150k | $30k | $20M | $10M |

| Early Employee #2 | $1/share | 75k | $75k | $12M | $10M |

State-level QSBS Applicability

References

- https://www.thetaxadviser.com/issues/2018/nov/qualified-small-business-stock-more-attractive.html

- https://www.svb.com/blogs/svb-private-bank/understanding-qualified-small-business-stock-the-capital-gains-exemption

- https://www.andersen.com/services/for-private-clients/business-owners-and-entrepreneurs/qsbs

- https://www.founderscircle.com/what-startup-founders-and-employees-need-to-know-about-qualified-business-stock-qsbs/

- https://www.parkworth.com/blogs/6-rules-for-exercising-stock-options-to-qualify-for-qsbs